The Essence of Know Your Customer – KYC Onboarding Process

Risks are inevitable. What distinguishes a successful company is its ability to handle and manage these risks effectively to foster growth and success.

Cybercrime is a particularly pervasive challenge. In 2023, the Federal Trade Commission’s (FTC) Consumer Sentinel Network recorded over 5.39 million reports, with 48 percent related to fraud and 19 percent to identity theft. This highlights a critical issue that businesses must address.

So, how can you protect your business from these issues? Let me tell you.

Do you Know Your Customer?

Did you know that if you’re a financial institution, you could face hefty fines, sanctions, and damage to your reputation if you engage in money laundering or terrorist financing? More importantly, you need to implement Know Your Customer (KYC) practices to protect your organization from fraud and financial losses caused by illegal activities and transactions. Now, how does the KYC onboarding process help in knowing customers?

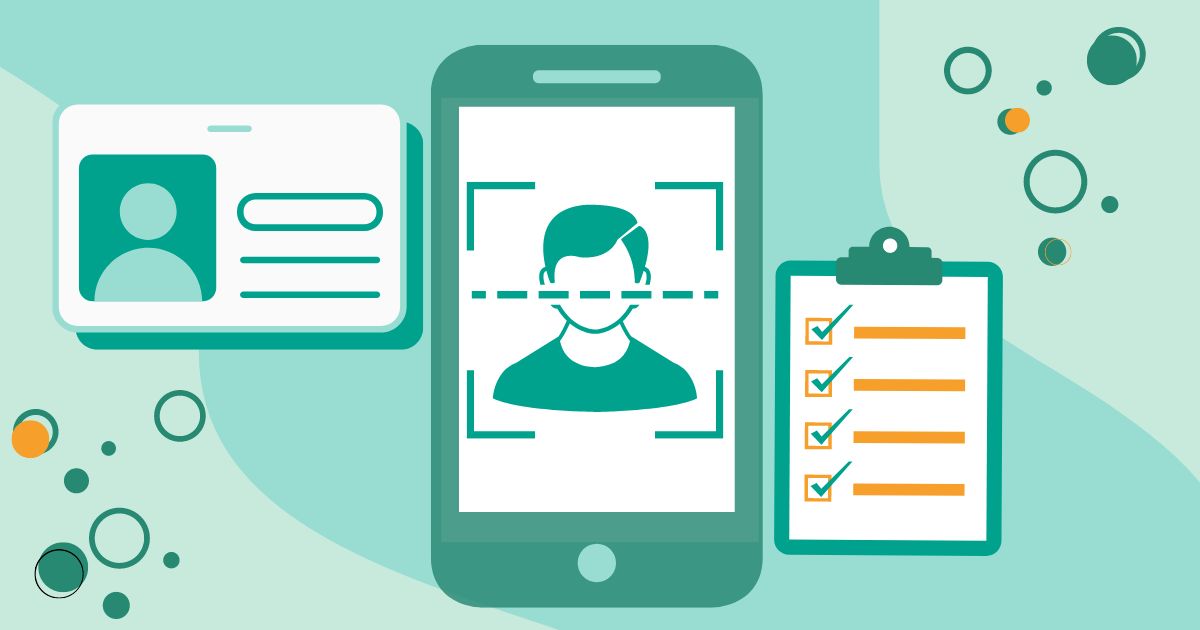

KYC onboarding is a step-by-step process used by businesses to confirm a customer’s true identity. It’s also known as Customer Onboarding or Client Onboarding. To protect the financial system, businesses must verify a customer’s identity right from the start.

While the specific steps of KYC onboarding can vary by country, all businesses need to collect and verify basic customer information such as:

- Name

- Date of Birth

- Proof of Address

Additionally, businesses often use unique identification numbers, like a Social Security Number or ID card number, to further confirm a customer’s identity. Once this information is collected and verified through a database, the customer can be successfully onboarded and start using the services.

Why Is KYC Onboarding So Important?

KYC onboarding is essential for industries that need to prevent money laundering and fraud. It helps verify the identity of new customers and assess their potential risk.

By following KYC procedures, businesses can avoid wasting time and resources on fraudulent or risky individuals. It also helps organizations understand if a customer might be involved in illegal activities like money laundering or terrorism financing.

In short, KYC onboarding is about being thorough and careful with new customers. It protects the business’s operations, reputation, and investment. A successful KYC onboarding process minimizes issues like false alarms and customer dissatisfaction, which can otherwise lead to losing customers.

The Perks of the KYC Onboarding Process

KYC onboarding offers several advantages for both organizations and their customers by reducing risks and streamlining operations. Here’s how:

1. Regulatory Compliance

KYC onboarding helps businesses meet legal requirements for verifying customer identities, ensuring they follow regulations like anti-money laundering (AML) procedures.

2. Market Insights

The information gathered during KYC helps businesses understand their market better. By checking applicants’ personal information against their digital activities, companies can gain valuable insights.

3. Streamlined Operations

Implementing KYC early helps organizations focus on key security issues and avoid problems that can arise from disorganized customer verification processes.

4. Enhanced Reputation

Conducting thorough KYC checks demonstrates to potential customers that the business prioritizes safety and compliance, boosting its reputation.

KYC onboarding not only ensures legal compliance but also improves operational efficiency and enhances the overall customer experience.

KYC Requirements for Customer Onboarding

The KYC (Know Your Customer) onboarding can vary based on a business’s needs and where it operates. However, there are two main requirements that must be met:

- Verify Personal Information: Make sure the customer provides all the necessary personal details and that this information is accurate and genuine.

- Screen and Assess: Evaluate the information to determine if the customer meets the KYC standards and can move forward in the process.

Here’s a simple four-step process for successful know your customer onboarding:

- Collect and Validate: Check that all required personal information (PII) has been received and is valid.

- Cross-Check Documents: Compare the PII with the customer’s photo ID and other documents to ensure they match.

- Conduct a Risk Assessment: Evaluate any potential risks or issues with the customer’s legitimacy. This helps us decide how closely to monitor the customer in the future for anti-money laundering (AML) or fraud prevention.

- Determine Eligibility: Based on the validated information and risk assessment, decide if the customer can proceed to the full KYC process. If there are issues, they might need further review but not necessarily be rejected outright. They could still become a customer after additional checks.

Eliminating Friction for a Smoother Customer Experience

The biggest issue with KYC onboarding is the friction it can create. No one wants to face delays or hassles when signing up with a new organization.

It’s not just customers who are affected; organizations also face challenges. According to McKinsey, banks spend up to 40% of their onboarding time on KYC and due diligence tasks. This can put a strain on their ability to smoothly welcome new customers.

If KYC onboarding isn’t done right, it can lead to unnecessary inconvenience. However, when done well, it can minimize customer hassles and save time.

Understanding and implementing KYC effectively is key to reducing friction. Token of Trust can help streamline the KYC process, making it easier for both organizations and their customers.

KYC Onboarding Like a Pro

Implementing an effective know your customer onboarding process is key to securing both your business and your customers.Start by selecting a digital KYC verification solution that fits your needs and integrates well with your current systems. Ensure you use a multi-layered verification approach, like biometric and document checks, to enhance security.

Also, educate your customers about the process to make their experience smoother and more straightforward. Following these best practices and using tools like Token of Trust, you can streamline onboarding, reduce fraud, and improve overall customer satisfaction.